By: Muhammad Zubair Mughal

There are more than 500 Islamic Microfinance instructions working in 44 countries of the world but funding has always been a critical issue in Islamic microfinance industry. Although Islamic microfinance with innovative product line and system has huge demand and acceptance across the world but the lack of funding can weaken its potential of growth in future and may hit the future expansion which can affect the financial inclusion strategy as Islamic Microfinance is an effective tool of financial inclusion for Muslim segment of the society who avoid conventional Microfinance due to religious reason as interest is strictly prohibited in Islam.

Unfortunately western donors are reluctant to provide funding to the Islamic microfinance industry which is diminishing its potential of growth, without adequate funding sources, Islamic Microfinance industry is facing lot of problems to serve the communities with better financial and non-financial services, so there is immense need of addressing such critical issues by introducing and developing the alternative source of funding for Islamic microfinance institutions to flourish this sector with full potential. Most of Islamic Microfinance Institutions are based on NGO’s or Charity Models but these are not enough to serve the 44% of the world poverty which is consist with Muslim world, we also need to introduce Commercial Islamic Microfinance MFI’s/Banks with handsome funding sources, some thematic guidelines and sources/models of funding for Islamic Microfinance institutions are given as under:

Sukuk – Social Sukuk:

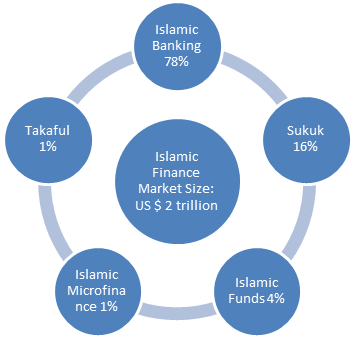

Sukuk refers to be the financing certificate similar to the bond but prohibiting to the interest/ non Shariah elements in its structure and mechanism. Generally Sukuk is utilized in the corporate sector for raising the funds for long term financing projects usually utilized for mega projects. The global volume of Islamic financial industry is about US $ 2 trillion in 2014 where Sukuk keeps 16% share and tends to be flourishing in foreseeable future providing Shariah compliant source of funding/ financing in Islamic Finance industry, it is expected the outstanding volume to reach $115 billion by year-end 2014.

As per the trends and norms in financial sector, Sukuk is considered and is utilized in corporate world only for mega projects but never experienced in Islamic microfinance industry to provide the funding source to Islamic Microfinance where it can be utilized effectively. Utilizing the Sukuk, Islamic microfinance industry can fulfill its needs of financing through Shariah compliant source of funding conforming the Shariah adherence in its both asset and liability sides. A new term “Social Sukuk” can be devised for such sukuk which is issued for social development and poverty alleviation projects.

Crowd Funding Platform:

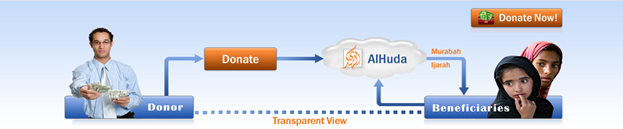

Crowd funding is the interlinked advanced online system, which can be utilized to generate funding opportunities for Islamic microfinance institutions and to overcome funding deficiencies, its run through an advanced system for transmission of funds to the beneficiary by linking the Microfinance institution and number of donors sitting in different parts of the world. Fortunately, there are number of donors and their majority is willing to socially lend/donate the funds for the charitable purposes, micro financing and especially to Islamic Microfinance institutions but the main hurdle is the transmission of funds but it can be addressed through better IT integration for connecting donors/ funds providers and IMFIs around the globe through different trustworthy payment gateways. Crowd funding platform will not only help to provide the funds for IMFIs rather it could be helpful in increasing outreach of Islamic Microfinance and allied services.

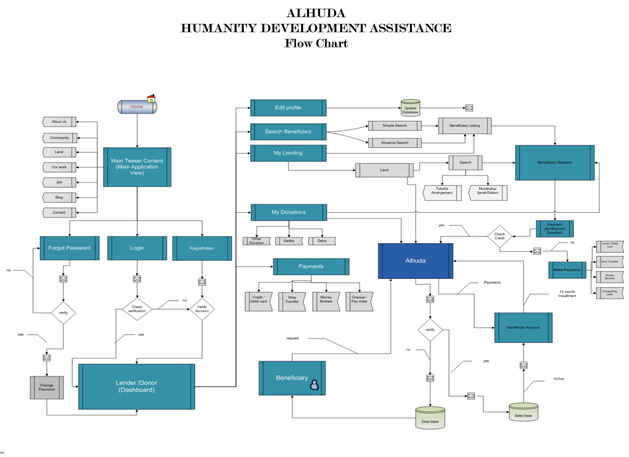

An Islamic Microfinance Crowd funding Architecture is as under:

Venture capital is a pool of funds which is generated by developed financial institutions through their surplus funds for best investment solution and profit motives. Venture Capital is usually utilized to start up, so Islamic Microfinance Institutions can also be developed through venture capital in Shariah Compliant manners. The venture capital can adequately be utilized in Islamic Microfinance to provide the source of funding to IMFIs where IMFIs can offer range of IMF products and services with institutional growth and sustainability in return, profit can be shared with capital providers. Equity financing is a technique of financing in which company issues shares of its stock and receives money in return or invest in any business venture as equity share holder. Venture capital is one of the more popular forms of equity financing. The equity fund can be categorized into three major categories i.e Microfinance development funds, Quasi-commercial microfinance investment funds, Commercial microfinance investment funds. In Islamic Point of view, Islamic Microfinance institutions can raise their funds through Equity Financing or Venture capital by utilizing Mudaraba or Musharaka mechanism. We can also observe that a plenty of Shariah compliant equity fund is also available in Islamic financial industry which is an motivational factor to introduce a equity fund for the development of Islamic Microfinance industry which facing a savior problem of funding.

Donor Grants, Soft Loans & Govt. Subsidies:

Donor Grants, Soft loans and Govt. Subsidies play a vital role for the development of Microfinance sector, but unfortunately, it is observed that International donor agencies are bit reluctant for Islamic Microfinance, therefore, Islamic Microfinance institutions are limited and facing expansion problems but in recent past we have seen that multilateral donor agencies are taking interest for the promotion of Islamic Microfinance as tool of financial inclusion and social development like Islamic Development Bank, GIZ, USAID, UKAID, IFAD and other agencies. Recently, the Govt. of Pakistan provides Qarz-e-Hassan (Soft Loans) to Islamic Microfinance institutions and we can also see such strategies in Yemen, Sudan, Indonesia and some other countries. So, this type of funding can play a pivotal role for fulfillment of funding limitation of Islamic Microfinance institutions/Banks.

Institutionalized Zakat System:

Zakat can play an important role to supplement Islamic Microfinance institutions that are working as non-for-profit, No doubt, Zakat cannot be utilized purely for Microfinance activities but it can supplement the other component of IMFIs i.e. Micro Takaful, Health, Education and Capacity Building programs which, ultimately, for poverty alleviation and economic empowerment financially neglected segment of society. But it can be done if Zakat system would be centrally institutionalized by submitting in a pool/ account from where it can be utilized for strengthened the Islamic Microfinance institutions.

Charity Funds or Penalty in Islamic Banking and Financial Institutions:

The charity amount as collected by Islamic Banks and Financial institutions all over the world consists of huge amount which is utilized in different charitable purposes but never utilized in Islamic Microfinance to address the funding need of IMFIs. Further, rectifying the misunderstanding, it is explicitly stated that there is no concept of penalty in Islam in financial arrangements/ commitments but as per the need in Islamic financial sector it is mandatory to fix a certain penalty to discourage the malpractices of delay in payments or willful defaults by the clients. This act keeps the financial sector at safe side from willful defaults or delay in repayment. So the collected amount of charity can be utilized in IMFIs as a source of funding or Qarz-e-Hassan (soft loan) for IMF services to alleviate poverty and to generate the economic activity which is not practiced yet and deems to be the quite appropriate approach/ model to address the funding issue of Islamic Microfinance Industry. Similarly, Institutional Penalty Fund means any penalty imposed on Islamic Financial institution for violation of Shariah compliances in the Islamic financial products and arrangements. As per the Shariah Audit, if it is proved by the Shariah auditor then the whole for partially income or amount, generated from such Islamic Banking product/s or operations, subjects to penalty and transferred, for charitable purposes and which may be utilized by Islamic Microfinance Institutions for supplementing their Microfinance operations and services.

Less Commercial Approach in Islamic Banking Institutions:

The size of Islamic finance industry will be approximately US $ 2 trillion in 2014 where share of Islamic Banking is about 78% and the global volume of Islamic Microfinance Industry is about US $ 1 billion but unfortunately its share is less than 1% in Islamic finance industry, which is a big question mark as well in Islamic finance that why Islamic Microfinance have less than 1% share in it. As the matter is concerned, it is stated that the Islamic microfinance can grow if Islamic banks and financial institutions have less commercial approach and design effective course of actions for the development of Islamic Microfinance industry by introducing different Shariah compliant financing modes to provide funds to the Islamic Microfinance Institutions or directly to poor as Islamic Microfinance product for the poverty alleviation and social development.

It is an arrangement where Islamic Microfinance institution can take funds on Mudaraba basis from Islamic Banks or Financial Institution. The Islamic Bank/ Financial Institution is the financier/ investor “Rabul Mal” and IMFI acts as investment manager “Mudarib” and IMFI does micro financing as per the Shariah principles and shares the profit with the investor (Islamic Bank/ Financial institution) as per the agreed ratio but in case of loss the loss is suffered by investor until the ignorance of Fund Manager (IMFI) is proved. While in Musharaka model both the parties (IMFI and Islamic Bank/ Islamic Financial Institution) provide funds for Islamic Micro Financing and share the profit, if generated, as per the agreed ratios but in case of loss the loss is also suffered by both the parties as per their ratio of investment/ contribution. The Mudaraba model is quite compatible for funding to the Islamic Microfinance institutions keeping both sides (asset and liability) Shariah compliant of IMFI. Currently it is being practiced by some Islamic Financial institutions with no harmful consequences. The proposed structure of Mudaraba model is given below:

Mudaraba Model for Islamic Microfinance Institution

Musharaka Model for Islamic Microfinance Institution

The term Waqf literally means "confinement and prohibition" or causing a thing to stop or stand still. The legal meaning of Waqf according to Imam Abu Hanifa, is the detention of specific things in the ownership of waqf and the devoting of its profit or products "in charity of poor’s or other good objects" (Wikipedia). The Concept of Waqf can also be utilized for the development of Islamic microfinance institutions where a particular property/asset or wealth or/and income can be endowment for socioeconomic development programs i.e. poverty alleviation through different Shariah compliant modes of Islamic microfinance, health or education programs for the poor’s etc. It is not mandatory in Waqf that the benefit/ income generated from the Waqf property shall be used for the charitable purposes only rather it gives an option to deal with Islamic microfinance effectively through different other trade based, partnership based and rental based Islamic microfinance products to generate income for institutional sustainability and Social development.

( Muhammad Zubair Mughal as a Chief Executive Officer of AlHuda Centre of Islamic Banking and Economics (CIBE) has been working consistently for last fifteen (15) years for poverty alleviation through Islamic Microfinance concept; he can be reached at zubair.mughal@alhudacibe.com )